In October 2024 the UK became the only country in the world to legally require banks to refund most authorised push payment (APP) scam victims — the person tricked into sending money gets reimbursed, and the sending and receiving banks split the bill up to £85,000. One year in, an independent evaluation by Frontier Economics for the Payment Systems Regulator (published 1 July 2026) found it worked: roughly £73 million a year less stolen, about 34,800 fewer scam cases, and none of the market collapse critics had predicted. But the protection is uneven — outcomes still vary sharply between banks — and two of the fastest-growing kinds of fraud, cryptocurrency and international transfers, are left out entirely.

What the law actually forces banks to do

For years the standard answer to “my bank won’t refund my scam” was a shrug: you authorised the payment, so you were on the hook. Voluntary codes existed, but banks applied them however they liked, and most victims of authorised push payment fraud — where you are manipulated into sending the money yourself — got nothing back.

On 7 October 2024 the UK replaced the shrug with a rule. Under the Payment Systems Regulator’s reimbursement requirement, banks and payment firms must refund victims of in-scope APP fraud: money you were deceived into sending by bank transfer over the Faster Payments or CHAPS systems. The cost is split 50/50 between the bank that sent the money and the bank that received it — which gives the receiving bank, the one that opened the account for the scammer, a direct financial reason to stop mule accounts. The guarantee runs up to £85,000 per claim. There is exactly one way out for a bank: it can refuse only if it can show the customer acted with gross negligence, a deliberately high bar that means far more than being careless.

No other country has made reimbursement mandatory like this. Our own Scam Refund Index, which grades 27 countries on what victims are actually owed, found the UK standing alone at the top — the single jurisdiction where a refund is a legal right rather than a goodwill gesture. That is what makes the first year of data worth reading closely: it is the only real-world test of whether forcing banks to pay actually works.

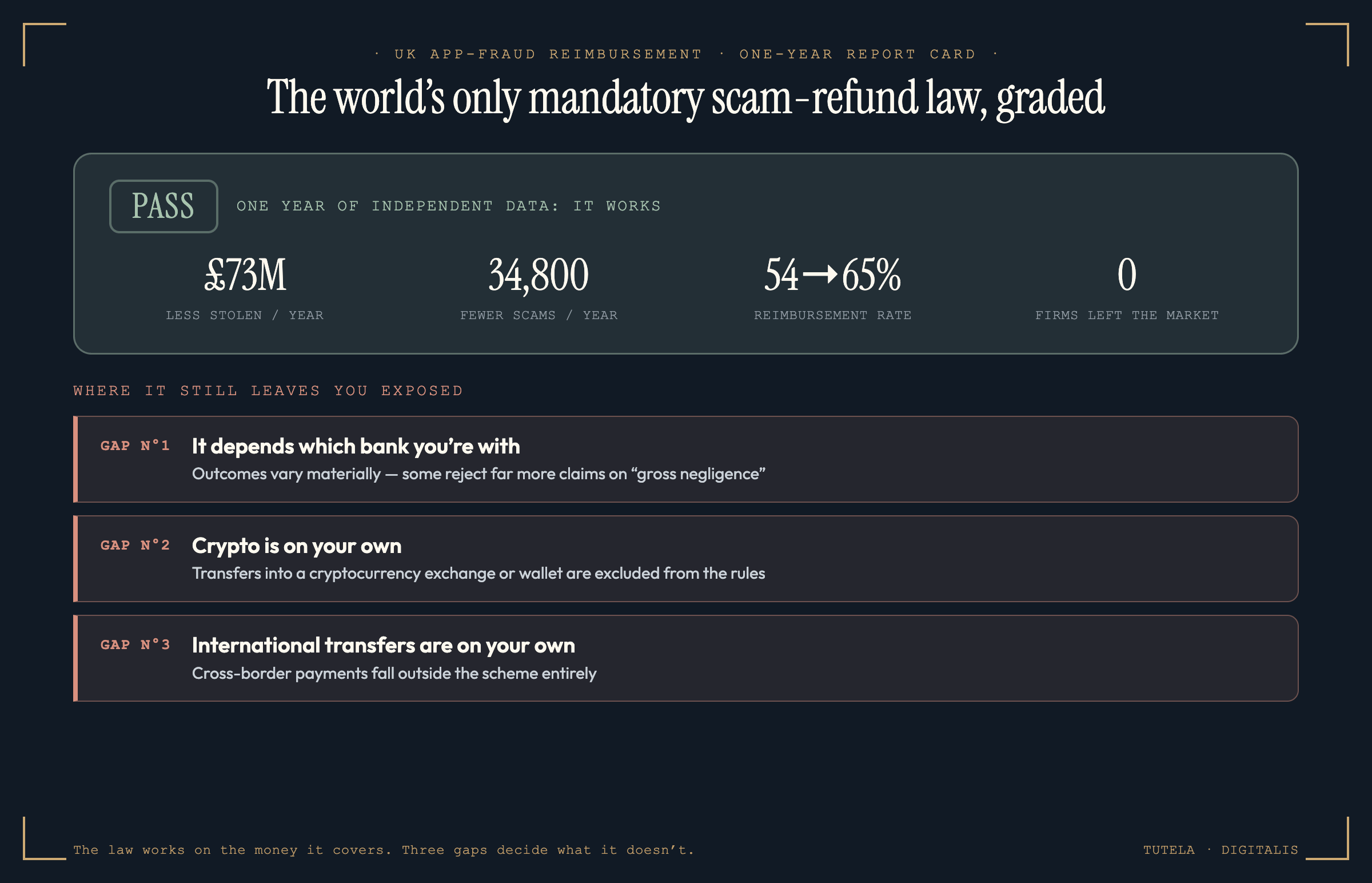

The verdict: one year of data says it works

On 1 July 2026, Frontier Economics published its independent evaluation, commissioned by the Payment Systems Regulator. The headline finding is that the rules did what they were meant to do. Consumer losses to APP fraud fell by an estimated £73 million a year, and the number of scams dropped by roughly 34,800 cases a year. Losses sent over the Faster Payments system — the main rail scammers use — fell about 21%.

The protection reached more people, too. Across all fraud claims, reimbursement rates rose from 54% to 65%; for claims that fall squarely inside the policy’s scope, firms now return the money in about 97% of cases. The rules cost banks an estimated £44–56 million a year to run — fraud prevention, claims handling, disputes, reporting — but the evaluation concluded the benefits exceeded those costs in the first year.

Perhaps the most important results are the two things that did not happen. Critics of the policy had two loud predictions: that forcing banks to pay would drive smaller firms out of the market, and that guaranteed refunds would make people reckless with their money. The evaluation found no evidence of either. No firms exited, and there was no sign of consumers taking more risks because they expected to be bailed out. The core objection to mandatory reimbursement — that it is unworkable and creates moral hazard — did not survive contact with the data.

Three gaps the first year exposed

A working law is not a complete one. The same evaluation that vindicated the rules also mapped their edges — the places where a UK scam victim can still end up with nothing. There are three, and they are worth knowing before you need them.

The rules are the same for every bank, but the enforcement is not. The evaluation found outcomes still "vary materially" between firms — some are far more likely than others to reject a claim by arguing the customer was "grossly negligent," the one exception the rules allow. Two people scammed the same way, on the same day, can get opposite answers depending only on who they bank with. Reimbursement rates rose from 54% to 65% across all claims, and hit 97% for claims squarely inside the policy — but the gap between the best and worst banks is where victims still fall through.

The reimbursement rules cover authorised push payments made over the UK's Faster Payments and CHAPS systems — an ordinary bank transfer you were tricked into sending. They do not cover money you moved into a cryptocurrency exchange or wallet. That is a large hole, because the fastest-growing, highest-loss frauds — investment "trading platform" scams and pig-butchering — are engineered specifically to route your money through crypto, which is exactly the leg the rules leave out.

The rules also stop at the border. A payment sent abroad — an international wire, a transfer to an overseas account — is outside the scheme. Romance and relationship scams frequently end with the victim wiring money internationally "to help" someone, and those transfers do not qualify for mandatory reimbursement. The protection is real, but it is a domestic-transfer protection.

Why this matters if you’re not in the UK

For everyone outside the UK, this first year of data is the answer to a question regulators have been circling for a decade: if you force banks to refund scam victims, does the system break? The honest, evidence-based answer is now on the table — no. Losses fell, more victims were made whole, banks kept operating, and consumers did not turn reckless. The UK ran the experiment; the rest of the world can read the result.

That matters because change is coming elsewhere. The EU’s incoming payment-services reforms are moving toward stronger reimbursement duties, and other regulators are watching the British numbers closely. When your own country’s banks tell you a refund mandate is impossible or dangerous, there is now one place on earth where it has been tried and measured — and the measurement disagrees with them. Until your jurisdiction catches up, the practical lesson from the UK’s gaps travels everywhere: the money that even the world’s strongest refund law cannot reach is crypto and cross-border transfers. Treat those two rails as unprotected wherever you live.

If a UK bank rejected your scam claim

The single most useful fact from the whole report is this: in-scope claims are now reimbursed about 97% of the time. So if your loss was an ordinary UK bank transfer you were tricked into sending, a refusal is the exception, not the rule — and it is very often reversible.

The verdict, in one line

The world’s only mandatory scam-refund law passed its first exam: on the money it covers, it works — less stolen, more victims repaid, no market collapse. What it still doesn’t cover is the money scammers work hardest to reach: crypto and international transfers. Know which side of that line your payment is on before you send it.

Sent money to a scammer and your bank said no? Let’s look at the claim together.

Tell us the amount, how you paid, and what the bank said. A real expert reviews every case and replies within 24 hours. Free, confidential, no pressure.

Common questions about the UK scam refund rules

Does my UK bank have to refund a scam?

In most cases of authorised push payment (APP) fraud, yes. Since 7 October 2024, UK banks and payment firms are legally required to reimburse victims who were tricked into sending money by bank transfer over the Faster Payments or CHAPS systems. The sending bank and the receiving bank split the cost between them, up to £85,000 per claim. There is one narrow exception — the bank can refuse if it can show you were "grossly negligent," which is a deliberately high bar, not simply "you should have known better." One year in, an independent review found firms now reimburse 97% of claims that fall squarely inside the scheme. The gaps are the money that falls outside it: cryptocurrency and international transfers are not covered.

How much can I get back under the UK reimbursement rules?

Up to £85,000 per claim. If you were tricked into sending an in-scope UK bank transfer, your bank must reimburse you up to that cap, and the receiving bank shares the bill. Some banks voluntarily refund above the cap, but £85,000 is the level the rules guarantee. You may be asked to pay a small excess of up to £100 in some cases, and vulnerable customers are exempt from the excess. The cap covers the large majority of individual scams — it is the crypto and international exclusions, not the ceiling, that leave the most money unprotected.

My bank said I was negligent and refused to refund — what can I do?

Do not treat the refusal as the end. "Gross negligence" is a high legal bar — it means far more than being careless or ignoring a warning; a scam being convincing is not negligence. The one-year evaluation found outcomes vary materially between banks precisely because some reject claims on this basis too readily. Ask the bank for its specific reason in writing, then escalate free to the Financial Ombudsman Service, which reviews the decision independently and overturns bank refusals regularly. The Ombudsman is free, and using it does not cost you your claim.

Are cryptocurrency scams covered by the UK refund rules?

No. The mandatory reimbursement rules cover authorised push payments over Faster Payments and CHAPS — ordinary UK bank transfers. Money you moved into a cryptocurrency exchange or wallet is outside the scheme. This is the single biggest gap, because investment-platform scams and pig-butchering are built to funnel your money through crypto, which is exactly the step the rules do not protect. If a "trading platform," an online partner, or a support agent is steering you toward buying crypto, treat it as outside the safety net completely.

Are international transfers covered?

No. The reimbursement rules apply to domestic UK transfers. Payments sent abroad — international wires or transfers to overseas accounts — are not in scope. Romance scams in particular often end in an international transfer, and those are not guaranteed a refund. Before sending money abroad to anyone you have not met in person, assume there is no reimbursement backstop behind it.

Did the UK's mandatory reimbursement rules actually reduce fraud?

Yes, according to the independent evaluation. Frontier Economics, commissioned by the Payment Systems Regulator and published on 1 July 2026, estimated the rules cut consumer APP-fraud losses by roughly £73 million a year and reduced scams by about 34,800 cases a year, with losses over Faster Payments falling around 21%. Just as notably, the two things critics predicted did not happen: no firms left the market, and there was no evidence of people behaving more recklessly with their money because they expected a refund. The policy's costs to banks were exceeded by its benefits in the first year.

Sources & further reading

Every figure in this piece is drawn from these authorities. Click any of them to verify.