The fake bank-advisor call — faux conseiller bancaire — is someone posing as your bank's fraud department who talks you into "protecting" your money by reading out a code, validating a payment, or moving funds to a "safe account." It is convincing in 2026 because, after the 2024 breaches at Free (around 5 million IBANs exposed) and France Travail (some 36.8 million people), the caller often already has your real name, address and IBAN. The one rule that defeats it: your real bank will never ask you to move money to another account, read out a one-time code, or validate a payment over the phone. If a caller asks for any of those, hang up and call your bank back on the number printed on your card.

If you have already moved money or validated a payment and want the emergency steps, skip to if you already paid. With a live transfer, minutes decide whether you see it again.

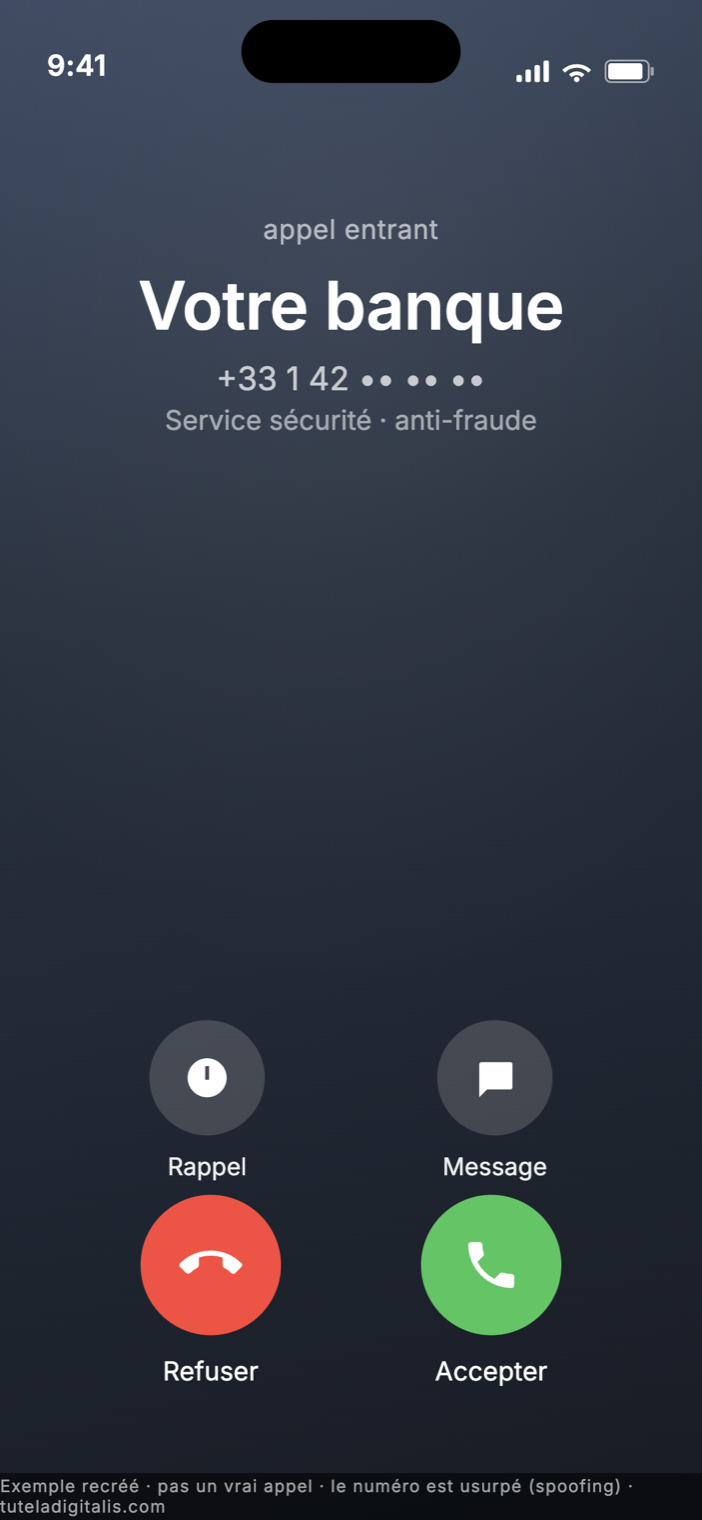

For years, the advice against phone scams was "your bank will never call you out of the blue." Criminals adapted, and the modern faux conseiller bancaire is built precisely to survive that instinct. The caller is calm, professional, and — this is the new part — armed with information only your bank should have. They are not fishing for your details. They are reciting them back to you to earn your trust, then using that trust to make you do the one thing that actually empties the account.

Why the call is so convincing now

The fuel for the 2026 wave was poured in 2024. French organisations were breached on an industrial scale: the telecoms operator Free confirmed attackers reached data for roughly 24 million customers, including about 5 million IBANs, and France Travail, the public employment agency, reported a breach touching some 36.8 million people. Names, addresses, dates of birth, phone numbers, account numbers — all of it circulating.

Hand a scammer that data and the script writes itself. They open with your real name and address, "confirm the last digits of your IBAN" to prove they're really your bank, and only then introduce the emergency. By the time the frightening part arrives, you have already filed them under "genuine." The scale is on the record: the Banque de France's Observatoire de la sécurité des moyens de paiement put total payment fraud at roughly €1.2 billion in 2024, and Cybermalveillance.gouv.fr's 2024 report logged more than 420,000 assistance requests (+49.9%) — with the fake bank-advisor scam up 78% and singled out as a defining threat. The data breach and the bank call are two ends of the same machine.

How the call actually goes

Almost every faux conseiller bancaire call follows the same arc, because it works:

The one thing your real bank will never do

Strip away the theatre and the whole scam rests on getting you to do something no genuine bank will ever ask of you by phone. Your bank will never ask you to:

If a caller asks for any one of those, you do not need to work out whether the rest of the call was genuine. The request alone is your answer. Hang up.

How to shut it down

If you already paid — the emergency steps

If you moved money, read out a code, or validated a payment, treat it as live and move in this order:

The one rule

If you take one habit from this piece, take this: no genuine bank ever asks you, by phone, to move money, read a code, or validate a payment. Hang up and call back on the number printed on your card. The caller who already knows your IBAN knows it because it was stolen — not because they're your bank.

Got a call like this — and not sure what you said? Tell us before you panic.

Describe the call and what you shared. A real expert reviews every case and replies within 24 hours — free, confidential, nothing to sell.

Common questions about the faux conseiller bancaire scam

What is the faux conseiller bancaire scam?

It is the fake bank-advisor scam: a caller pretends to be from your bank's fraud or security department, says your account is under attack, and talks you into 'protecting' your money — by reading out the codes your bank texts you, validating a payment in your app, or moving funds to a 'safe account' that belongs to the criminal. France's cyber-victim platform Cybermalveillance.gouv.fr has reported a sharp rise in this fraud. What makes the 2026 version so dangerous is that the caller often already has your real details — name, address, and even your IBAN — so the call sounds genuine from the first second.

How do the scammers already know my bank details?

From large data breaches. In 2024, French companies were breached on a mass scale — the telecoms operator Free confirmed attackers accessed data for around 24 million customers, including roughly 5 million IBANs, and France Travail (the public employment agency) reported a breach affecting some 36.8 million people. With your name, address, date of birth, phone number and IBAN circulating, a criminal can build a call that already 'knows' you. The data is the reason the script works.

Will my real bank ever ask me to move money to a 'safe account'?

No. This is the single most important rule. A genuine bank will never call and ask you to transfer your money to a 'secure' or 'holding' account, to read out a one-time code or validate a payment 'to cancel it', to give your full card number or passwords, or to install software so they can 'help'. Every one of those is the scam. If a caller asks for any of them, hang up and call your bank back yourself on the number printed on your card.

The number that called me was my bank's real number — how?

That is spoofing: software lets a caller display any number they choose, including your bank's or a public administration's. A matching number on your screen proves nothing. France has begun rolling out anti-spoofing authentication for calls, but you cannot rely on the displayed number to tell you a call is genuine. Treat the caller ID as decoration, not proof.

I already moved money or validated a payment — what do I do now?

Act in minutes, not hours. Call your bank immediately on the official number to report the fraud and ask them to block the transfer and freeze the account — under the French monetary code, an unauthorised payment you report promptly must in principle be refunded, though banks often resist when they argue you 'authorised' it, so report fast and in writing. If a bank card was used, file a Perceval report via service-public.fr; for other online fraud, use the THÉSÉE platform. Call Info Escroqueries on 0 805 805 817 for guidance, and France Victimes on 116 006 for support. Then ignore anyone who later offers to 'recover' your money for a fee.

Sources & further reading

Claims in this piece are attributed to these sources. Click any of them to verify.