For buying from someone you don't know, PayPal is the safest — but only because its Goods & Services option carries Purchase Protection, with a dispute window of up to 180 days. The safety comes from the payment type, not the brand: PayPal's own Friends & Family option has no protection, and Venmo, Cash App, and Zelle offer little to none on personal payments. If you authorize a payment to a scammer, only PayPal Goods & Services reliably gives you a way back. For sending money to people you already know, all four are fine.

If you just want the bottom line for a specific app, the comparison table below has it. But the reason the table looks the way it does is worth two minutes, because it's the thing that actually keeps your money safe.

The question is "which app?" The answer is "which payment type?"

Almost every "is PayPal safer than Zelle?" article ranks the apps like sports teams. That framing quietly misses the point, because the same app can be the safest or the riskiest way to pay depending on one choice you make at checkout.

There are really only two kinds of payment on these platforms:

Hold that distinction and the rest is simple: the safest payment is one you can dispute; the riskiest is one that acts like cash. The brand only matters because of which type it nudges you toward.

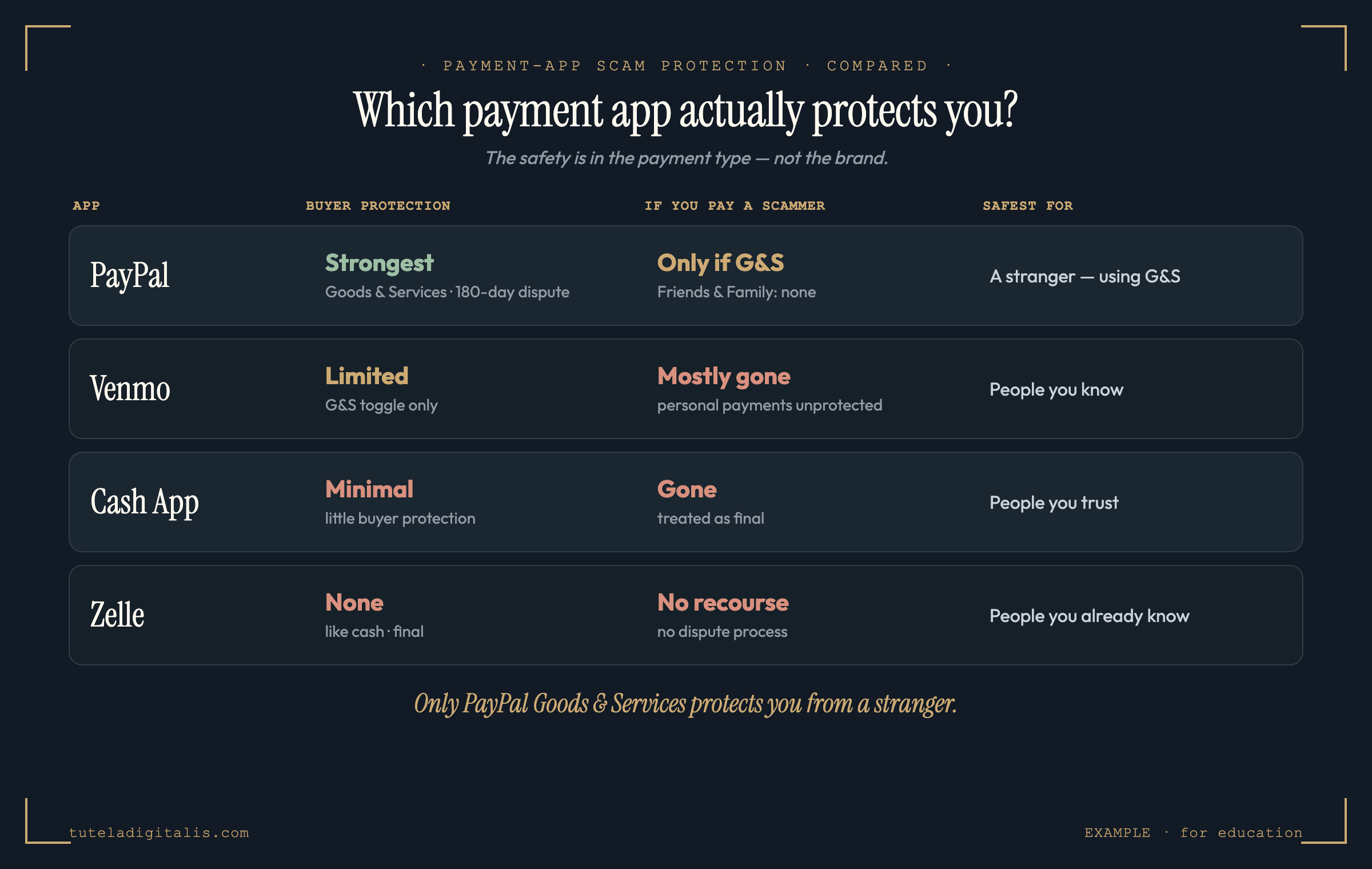

PayPal vs Venmo vs Cash App vs Zelle: scam protection compared

Here's how the four apps actually compare on the things that matter when a deal goes wrong — not features and fees, but whether you can get your money back.

| App | Buyer protection | If you authorize a payment to a scammer | Safest for |

|---|---|---|---|

| PayPal | Strongest Purchase Protection on Goods & Services; open a dispute up to 180 days after paying, and PayPal adjudicates. | Covered — if G&S If you paid as Goods & Services, you can claim. If you paid Friends & Family, you have no Purchase Protection. | Buying from someone you don't know — but only with the Goods & Services option. |

| Venmo | Limited Buyer protection applies only to eligible payments made with the Goods & Services toggle on; ordinary personal payments are not covered. | Mostly gone Personal (Friends & Family-style) payments have no buyer protection — the box almost every Venmo scam is engineered to land in. | Paying people you actually know. |

| Cash App | Minimal Cash App's own guidance is to send money only to people you know and trust; it offers little buyer protection for purchases. | Gone Authorized payments you send are treated as final; recovering them is rare. | Sending money to people you trust. |

| Zelle | None Zelle has no buyer/seller protection; payments are designed to be like cash — fast and final, with no dispute process. | No recourse Zelle itself says to use it only with people you know and trust; an authorized payment to a scammer typically can't be reversed. | Paying people you already know and trust. |

App by app: the honest version

PayPal has the strongest buyer protection of any major US payment app. Pay for an item with Goods & Services and you can open a dispute up to 180 days later; if it never arrives or isn't as described, PayPal can refund you. The catch is the other button: Friends & Family has no Purchase Protection whatsoever. So "PayPal is safe" is only half a sentence — PayPal is safe when you use Goods & Services.

Venmo (a PayPal-owned service) added a Goods & Services toggle that provides limited buyer protection on eligible purchases. But its default, and the way most people use it, is a personal payment — which carries no protection. Nearly every Venmo scam is engineered to land in that unprotected box.

Cash App offers little buyer protection. Cash App's own guidance is to send money only to people you know and trust. Treat a payment there the way you'd treat handing over cash — because for recovery purposes, it largely is.

Zelle has no buyer or seller protection by design. It moves money straight between bank accounts, fast and final, and Zelle's own advice is to use it only with people you already know and trust. That makes it excellent for repaying a friend and dangerous for paying a stranger — there is no dispute process to fall back on.

The trap hiding in plain sight: "send it Friends & Family"

This is the move to watch for. A seller, a "landlord," or a marketplace buyer asks you to pay by Friends & Family, a Venmo personal payment, Cash App, or Zelle — often framed as a favor, "to avoid the fee."

So which should you use?

It comes down to who you're paying.

The one line to carry: your protection lives in the payment type, not the app — and the safest payment is always the one you can dispute.

Already sent a payment that feels wrong? Don't wait, speed matters most.

If you just paid for something that smells like a scam, the next hour matters more than the shame does. Our free triage tool sorts your next steps by exactly how the money left.

Common questions

Which is the safest payment app — PayPal, Venmo, Cash App, or Zelle?

For buying something from someone you don't know, PayPal is the safest because its Goods & Services option includes Purchase Protection, with a dispute window of up to 180 days. But the safety comes from the payment type, not the brand: PayPal's own Friends & Family option has no Purchase Protection at all, and Venmo, Cash App, and Zelle offer little to none for personal payments. For sending money to people you already know and trust, all four are fine; for paying a stranger, only PayPal Goods & Services actually protects you.

Is PayPal really safer than Zelle?

For a purchase, yes — by a wide margin. PayPal Goods & Services lets you open a dispute and can refund you if the item never arrives or isn't as described. Zelle has no buyer protection and no dispute process; Zelle's own guidance is to use it only with people you know and trust, because payments are designed to be like cash — fast and final. So Zelle isn't 'unsafe,' it's just not built for paying strangers, and it gives you no way back if you do.

If I get scammed and I sent the money myself, will any app refund me?

Usually not — and this is the part people miss. When you willingly hit 'send' (an authorized payment), all four apps treat it as a transaction you chose to make. That covers fake-listing deposits, 'friend in trouble' requests, marketplace items that never arrive, and overpayment tricks. The one real exception is PayPal Goods & Services, whose Purchase Protection is built for exactly this. Friends & Family, Venmo personal payments, Cash App, and Zelle generally won't reverse a payment you authorized.

What's the difference between 'Goods & Services' and 'Friends & Family'?

It's the single most important setting on PayPal and Venmo. Goods & Services flags the payment as a purchase, which turns on buyer/Purchase Protection (and charges the seller a small fee). Friends & Family (or a Venmo personal payment) is meant for splitting a bill or repaying a friend — it's free, but it has zero buyer protection. Scammers constantly push buyers to use Friends & Family 'to avoid the fee.' That request is itself a red flag: it's really a request to remove your protection.

So how should I actually pay a stranger online?

If you must pay someone you don't know — a marketplace seller, a private sale, a deposit — use PayPal Goods & Services, or better still a credit card, which adds its own chargeback rights on top. Never use Zelle, Cash App, a Venmo personal payment, or PayPal Friends & Family with a stranger, and treat any seller who insists on those as a scammer. The safest payment is one you can dispute; the riskiest is one that behaves like cash.

Sources & further reading

Every claim here is drawn from each provider's own published terms and US consumer guidance. Click any to verify.