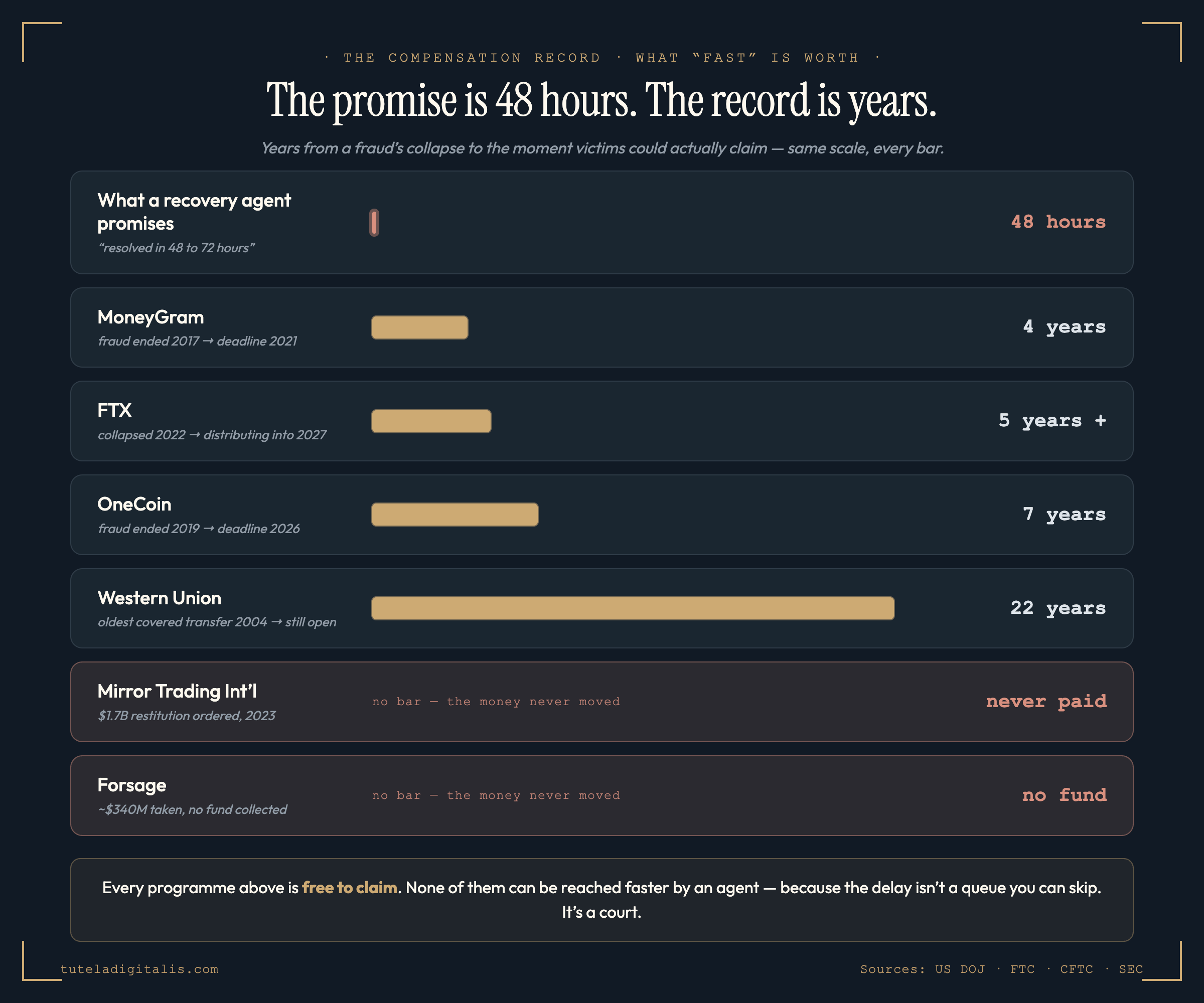

You can sometimes get scammed money back, but almost never quickly, and the speed is the part being sold to you. If your money went by ordinary bank transfer and you are in the UK, reimbursement is legally mandatory and takes days to weeks — and our Refund Index found the UK is the only one of 27 countries that requires it. For everything else — crypto, wires, gift cards, and bank transfers almost everywhere else — the honest measure is years. Of the eleven compensation programmes in our Compensation Tracker, exactly one is still open to new claims; OneCoin’s victims waited seven years from the fraud’s collapse to a claim deadline; Mirror Trading International’s $1.7 billion was ordered and never paid. Every legitimate route is free. Anyone charging you a fee to make it faster is running the second scam.

There is a reason the internet is full of listicles with this exact title, and it is not a coincidence of search engine optimisation. “5 easy steps to recover your money” is a sales page. It is the landing pattern of the fund-recovery industry, and the promise underneath it is always the same one: that the thing standing between you and your savings is a procedure you don’t know yet, and they do.

That is a lie, but it is a specific lie, and it is worth naming precisely. It is not a lie about whether the money can come back. Sometimes it genuinely can. It is a lie about when. Every real route back to your money is slow, unglamorous, free, and mostly out of your hands — which is exactly why nobody can build a business on it. The recovery scammer isn’t selling you your money. He is selling you the calendar.

So here are the five steps, honestly. One of them is easy.

The list, rewritten by someone who isn’t charging you

The people who took your money and the people now offering to get it back are frequently the same operation, working from the same spreadsheet. Being scammed once is the qualifying criterion for being scammed twice — your loss is what turned you into a lead. The FBI tracks recovery fraud as a category of its own precisely because it is that reliable. And every reply you send is not neutral: each confirmed detail, each emotional tell, each hour you stay in the conversation is data that sharpens the next approach on you.

We track eleven real compensation programmes for collapsed frauds. Every legitimate one is free. Not cheap — free. A US Department of Justice remission, an FTC redress fund, a bankruptcy trustee: none of them charges you to file, and none of them can be reached faster by an agent than by you. There is no queue to skip, because there is no queue. So an upfront fee is not one red flag among several. It is the whole diagnosis, and it does not matter how plausible the reason attached to it sounds.

This is the step that feels most futile and is quietly the most load-bearing, which is exactly why the recovery industry tells you to skip it. OneCoin collapsed in 2019; the Justice Department opened a remission portal with more than $40 million available for its victims in 2026. Western Union's $586 million fund is still accepting claims for transfers sent as far back as 2004. You are not filing to get paid this month. You are filing so that you exist in a record that might pay out in a decade — and nobody who wasn't in the file got anything at all.

There are two clocks, and almost everything depends on which one your money is on. If you sent an ordinary bank transfer and you're in the UK, you're on the fast one: reimbursement is legally mandatory, and an independent review found 97% of claims squarely inside the scheme are now paid. Our Refund Index checked 27 countries and found the UK is the only one that requires this. Everywhere else — and for cryptocurrency, wires and gift cards everywhere, including the UK — you are on the slow clock. That one is measured in years, and it frequently ends at zero.

Look at what the calendar actually says. OneCoin's fraud ended in 2019 and the claim window closed in 2026 — seven years just to be allowed to ask. MoneyGram's fraud ended in 2017; its deadline was 2021. FTX collapsed in 2022 and is still distributing into 2027, and it repays at the dollar value of the day it collapsed, not today's. Mirror Trading International has $1.7 billion ordered for its victims, and the CFTC itself cautions that an order may not result in actual recovery. Forsage's victims are owed nothing, from a fund that was never collected. Nobody should spend seven years refreshing a portal.

The arithmetic behind step 5

None of the above is a mood. It is what our own Compensation Tracker says when you read it as a clock instead of a directory. We built it to answer “is there a fund for my scam?” — but counted a different way, it answers a question nobody else seems to want to publish: how long does this actually take, and how much actually arrives?

Why “fast” is the entire fraud

Put those two facts next to each other and the con becomes legible. The real system moves in years. The victim needs the money this month — the rent, the retirement, the thing that was going to happen. That gap, between how fast you need it and how slow the machinery is, is not an unfortunate side effect of fraud. It is the product being sold in the second act.

This is why the recovery pitch never argues that the money is gone or not gone. It argues about speed. We work faster than the authorities. We can have this resolved in 72 hours. We’ve already located your funds. Every one of those sentences is aimed at the same nerve, and none of them is a claim about recovery at all. They are claims about the calendar, and the calendar is the one thing nobody — not the FBI, not the DOJ, not a bankruptcy trustee, not us — can compress for you.

The one exception, and press it hard

There is a real fast clock, and if you are on it, everything above should be ignored in favour of moving immediately. If you were tricked into sending an ordinary bank transfer in the UK, reimbursement has been legally mandatory since October 2024. An independent evaluation for the Payment Systems Regulator, published in July 2026, found that 97% of claims squarely inside the scheme are now reimbursed, and that the rules cut losses by roughly £73 million a year. That is days-to-weeks money, it is your legal entitlement, and it is the closest thing to a working refund system anywhere on earth.

The catch is how narrow the exception is. Our Refund Index checked 27 countries and found one that mandates reimbursement. And even inside the UK, the scheme stops at the edge of the banking system: crypto and international transfers are excluded, which is precisely where investment scams and romance scams are engineered to send you. If your bank refuses on “gross negligence,” that is not the end — escalate free to the Financial Ombudsman, which overturns those refusals regularly. But if your money was converted to crypto and moved, you are back on the slow clock with everyone else.

Step 5, one more time

The reason the honest list ends where it does isn’t cynicism, and it isn’t telling you your money doesn’t matter. File the report. File the claim if one exists. It is free, it costs you an afternoon, and it is the only mechanism by which a fund in 2033 could ever find your name. Do it properly and keep the paperwork.

Then close the tab. Because the seven years OneCoin’s victims waited were going to pass whether they spent them refreshing a portal or not, and the people who spent them refreshing were the ones still reachable when the second offer arrived. There is no diligence that makes a court faster. There is only a life continuing or not continuing while the machinery grinds.

That is the step the recovery industry cannot sell around, and the reason they need you to skip it. Their entire business is your refusal to move on. Moving on isn’t giving up on the money. It is the one move that makes you worthless to them — and it is the only step on this list that is genuinely, immediately, in your hands.

For journalists

The underlying data and the graphic above are free to cite and republish, with credit (CC BY 4.0). The one-line finding: of the eleven major fraud-compensation programmes we track, only one is still open to new claims; where the wait can be measured it runs four to twenty-two years from a fraud’s collapse to a claimable payout; and two have never paid a victim at all.

Every programme is sourced to a primary authority (DOJ, FTC, CFTC, SEC) and links to it. The elapsed times are derived from dates already published in those sources, never estimated — where no sourced fraud-era date exists, we publish no figure rather than guess, and the tracker says so on the row.

Suggested citation: The Tutela Digitalis Scam-Victim Compensation Tracker, June 2026 — tuteladigitalis.com/scam-compensation-tracker

Need the underlying programme-by-programme data, an updated figure, or a quote? Email press@tuteladigitalis.com.

Someone has offered to get your money back? Send us the message before you send them anything.

Tell us what you lost, how you paid, and what they’re asking for now. A real expert reviews every case and replies within 24 hours. Free, confidential, and we will never charge you to recover anything.

Common questions about getting scammed money back

How long does it actually take to get money back after a scam?

It depends entirely on which payment rail your money left on, and the two answers are far apart. If you sent an ordinary bank transfer in the UK, reimbursement is legally mandatory and is handled in days to weeks — an independent review found 97% of claims squarely inside the scheme are paid. That is the fast clock, and almost nobody is on it: our Refund Index checked 27 countries and the UK is the only one that requires reimbursement. For everything else — cryptocurrency, wire transfers, gift cards, and bank transfers in most of the world — the honest answer is years, if ever. Of the eleven compensation programmes we track, OneCoin's fraud ended in 2019 and its claim window closed in 2026; MoneyGram's fraud ended in 2017 and its deadline was 2021; FTX collapsed in 2022 and is still distributing into 2027. Anyone quoting you 48 to 72 hours for money that has already left the banking system is selling you something.

Do fund recovery services actually work?

No legitimate compensation programme requires one, and none of them can be accessed faster by an agent than by you. Every one of the eleven programmes we track — DOJ remission, FTC redress, court-supervised bankruptcy distributions — is free to file and open directly to victims. There is no queue to skip and no relationship to leverage. That is why an upfront fee is not a warning sign among others but the diagnosis itself: a service charging you to unlock money that is free to claim is either selling you nothing or is the second scam. The FBI treats recovery fraud as its own category because targeting people who have already lost money is one of the most reliable frauds running.

Is there a compensation fund for scam victims?

Sometimes — but far less often than people assume, and almost never quickly. We maintain a tracker of eleven programmes tied to collapsed frauds. Exactly one, the Western Union remission fund ($586 million, covering transfers from 2004 to 2017), is still accepting new claims from individual victims. Three crypto bankruptcies (FTX, Celsius, Voyager) are still distributing, but only to creditors who filed before their claims deadlines passed. Four programmes are closed. One, Mirror Trading International, is a $1.7 billion paper judgment with no active payout. One, Forsage, has no victim fund at all. Funds exist for a small minority of very large, very public frauds, years after the fact. Most scams never produce one.

Should I pay someone to recover my scammed money?

No. Every legitimate route is free, and payment is the mechanism of the second scam rather than an incidental detail of it. The rule that survives every story you will be told is that in a real recovery, money moves toward the victim. A request to send anything first — a processing fee, a legal retainer, a tax, a release charge, a small deposit to verify your wallet — ends the conversation regardless of how convincing the reason sounds or how official the person looks. Fraudsters running recovery scams impersonate law firms, regulators, and in some cases the FBI's own IC3 reporting centre.

Will I ever get my money back after being scammed?

Honestly: for most people, most of the time, no — and the sooner you know that, the safer you are. The exception is real and worth pursuing hard: if your money went by bank transfer, you may be inside a reimbursement scheme (mandatory in the UK, voluntary or absent almost everywhere else) and you should press that claim immediately, escalating to your ombudsman if the bank refuses. Outside that, the record is bleak. BitConnect returned more than $17 million to around 800 victims of a roughly $2.4 billion scheme. Forsage's victims got nothing. Mirror Trading International's $1.7 billion was ordered and never paid. What that arithmetic should change is not whether you file — you should, it's free and it's the only thing that could pay out later — but whether you organise your life around waiting.

Why do scammers target people who have already been scammed?

Because a proven victim is a qualified lead, and the industry is organised around that fact. Your details circulate on what fraud investigators call sucker lists — records of who lost money, how much, and how they paid. The second approach then arrives already knowing the answers, which is what makes it credible: it names your real loss, your real platform, your real amount. That is not clairvoyance, it is a database. The FBI logs recovery fraud separately for this reason, and it warns that fraudsters impersonate its own IC3 centre to run it. If someone contacts you unprompted and already knows what happened to you, that knowledge is evidence against them, not for them.

Sources & further reading

Every figure in this piece comes from these authorities, and every one of them is free to read. Click any of them to verify.