Poland's routes in 2026: call your bank's fraud line the same hour to try to block the transfer or freeze the receiving account. Report the incident to CERT Polska (the national CERT, run by NASK) at incydent.cert.pl, and forward a scam SMS free to 8080. Report the crime to the police — call 112 or file a zawiadomienie at a local unit or prosecutor. For a bank-refund dispute, go to the Rzecznik Finansowy (Financial Ombudsman); for a suspicious investment firm, check and report it to the KNF warning list; for consumer issues, UOKiK. There is no single national portal. And the hard part: an unauthorised payment must be refunded, but a BLIK code or transfer you were deceived into approving generally is not.

If you've just been scammed in Poland, the first hours come down to two things: giving the bank a chance to stop the money, and building a record while the evidence still exists. The order below is the fastest path through a system that has no single front door.

If you're reading this with a transfer you already regret, skip to if money has already moved — a fast call to your bank is sometimes the only thing that works.

The hard truth about getting your money back

This matters most, because it sets your expectations correctly before you spend a week chasing the wrong outcome.

Polish law follows the EU baseline through the Payment Services Act (the ustawa o usługach płatniczych, which implements PSD2). If a payment was unauthorised — made without your consent, like a stolen credential used without you — the bank must refund it, and you have up to 13 months from the debit to claim. If you authorised the payment yourself while being deceived — you generated and confirmed a BLIK code, or made the transfer — that counts as a valid instruction, and the automatic refund right does not apply.

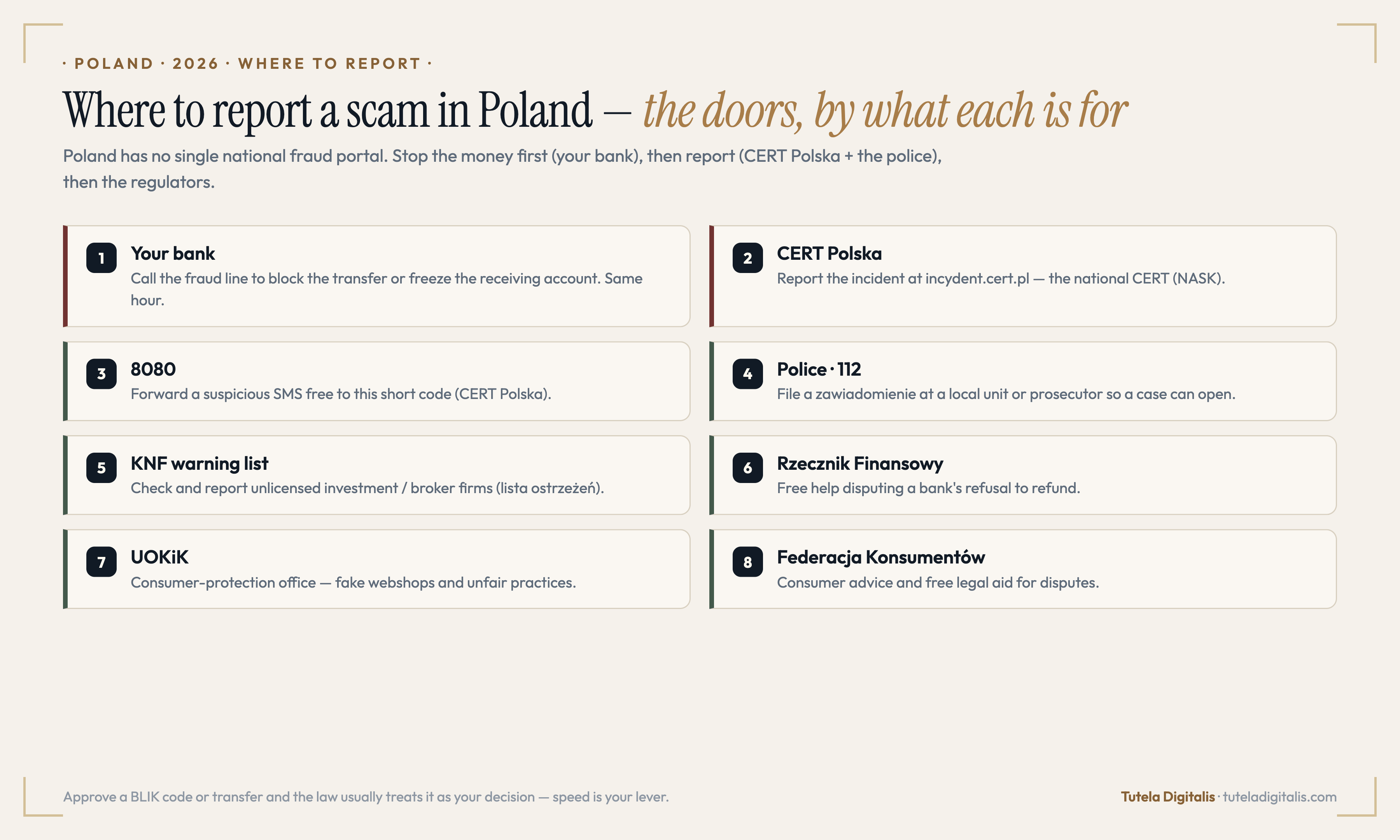

Start with your bank, CERT Polska and the police

Three reports matter most, and the order is the same every time: the bank moves on the money, CERT Polska handles the technical side, the police open the criminal case.

The full Polish reporting directory, by scam type

Different scams route to different specialists. Using the right one matters more than reporting to all of them.

If money has already moved — the first hours

Speed is the whole game. This is the maximum-recovery order:

The habits that keep you out of the reporting machinery entirely

Reporting is downstream. Prevention is upstream, and three habits stop most Polish scams cold:

If you're unsure whether something is a scam before any money moves, the fastest second opinion is the Scam Checker on this site, or our free case review. Both are read by a human and answered within 24 hours.

One rule, end to end

If you take one habit from this piece, take this: any unsolicited call, message, or "friend" that pressures you to move money, approve a payment, or share a BLIK code is a scam until you have verified it by contacting the person or your bank back on a number you already trust. Poland will help you report it after the fact — but the pause that stops the transfer is still worth more than every authority downstream of it.

In Poland and not sure where to start? Let's look at it together.

Describe the message, the call, the transaction. A real expert reviews every case and replies within 24 hours. Free, confidential, no pressure.

Common questions about reporting a scam in Poland

Where do I report a scam in Poland?

Move on two fronts in the same hour. First, your money: call your bank's fraud line to try to block the transfer or freeze the receiving account. Second, the report: file the incident with CERT Polska — the national CERT run by NASK — at incydent.cert.pl, and report the crime to the police (call 112, or file a zawiadomienie o przestępstwie at any local unit or prosecutor's office). You can forward a suspicious SMS free to the short code 8080. There is no single national 'report cybercrime online' portal like the UK's, so reporting runs through CERT Polska plus the police in parallel.

Will a Polish bank refund a BLIK or transfer scam?

It turns on one distinction. Under the Polish Payment Services Act (the ustawa o usługach płatniczych, which implements the EU's PSD2), banks must refund unauthorised transactions — payments made without your consent, like a stolen credential used without you. But if you authorised the payment yourself — you generated a BLIK code and confirmed it, or made the transfer — banks treat it as a valid instruction, and authorised payments you were deceived into are generally not refunded. You have up to 13 months from the debit to raise an unauthorised-transaction claim. Chargeback does not apply to BLIK or bank transfers, so be wary of anyone who promises an easy reversal.

What is the difference between CERT Polska, the police, and KNF?

They do different jobs. CERT Polska (NASK) is the national cyber-incident team — report phishing sites, malicious domains and incidents at incydent.cert.pl, and forward scam SMS to 8080; it handles the technical side and blocking, not your money. The police (Policja) investigate the crime — file a report so a criminal case can open. KNF, the financial regulator, publishes a public warning list (lista ostrzeżeń publicznych) of suspected illegal financial and investment operators — check it before investing, and report a suspicious firm to ostrzezenia@knf.gov.pl. For a refund dispute with your bank, the Rzecznik Finansowy (Financial Ombudsman) is the body that helps.

Someone is offering to recover my lost money for a fee — is that legitimate?

No — that is the second scam, and it targets people who have just lost money. Fake 'recovery' agents, bogus lawyers, and people impersonating the police, your bank or KNF will promise to get your money back for an upfront fee, a 'commission', or your banking details. No genuine Polish authority or service charges you upfront to recover funds. Block them, and check anything you are unsure about with your bank or with us first.

I got a fake bank or parcel SMS in Poland — what do I do?

Treat it as a scam and don't tap the link. Fake bank 'security' texts, fake parcel and InPost delivery messages, and fake court or mObywatel notices are among the most common in Poland. Open your bank's official app yourself rather than any link, and never approve a payment or share a BLIK code because a message told you to. Forward the suspicious SMS free to 8080 (run by CERT Polska), and report a phishing site at incydent.cert.pl. If money was lost, call your bank and report to the police.

Sources & further reading

Claims in this piece follow CERT Polska (NASK), KNF, and the Rzecznik Finansowy, with reporting channels as published by the authorities. Click any to verify.