OneCoin was a fake cryptocurrency sold from 2014 as the next Bitcoin. It was not a cryptocurrency at all: U.S. prosecutors say it had no real blockchain — the "coins" were entries in a private company database, the price was set by the company, and it was never listed on a legitimate exchange, so members could almost never sell. The U.S. Department of Justice calls it one of the largest fraud schemes ever charged, with worldwide losses of more than $4 billion. Founder Ruja Ignatova vanished in 2017 and is on the FBI's Ten Most Wanted list; co-founder Sebastian Greenwood got 20 years, and the lawyer who laundered the money got 10. If you lost money, one free, legitimate recovery route now exists — the U.S. DOJ remission, due 30 June 2026.

For a few years OneCoin was everywhere — sold in hotel ballrooms and over WhatsApp, pitched by friends and relatives, marketed with the confidence of a tech revolution you were lucky to get in on early. The promise was simple: this is the next Bitcoin, and you can still buy in before the price explodes. Millions of people believed it. The trouble is that none of the machinery underneath the promise was real.

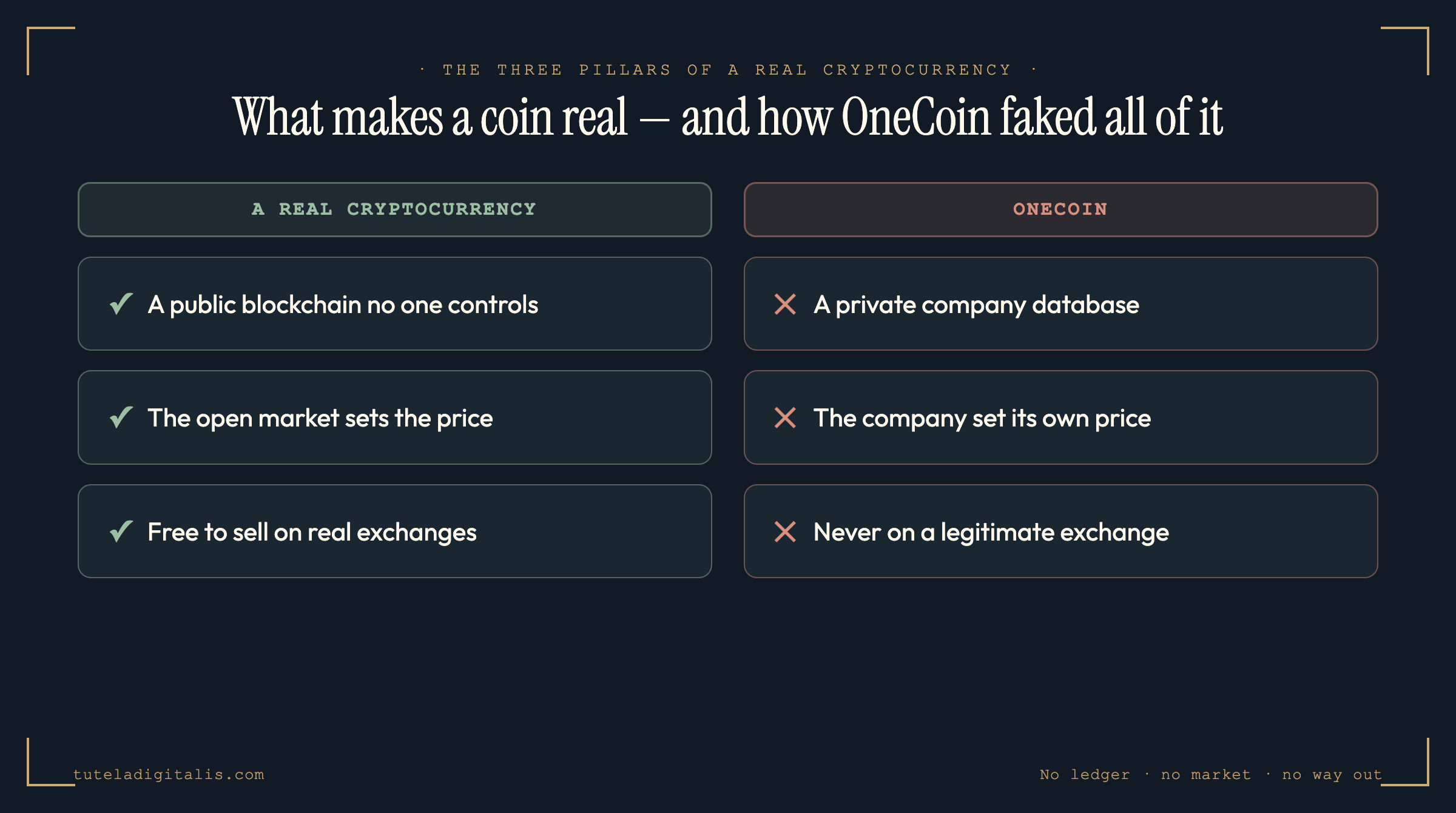

If you only remember one thing about OneCoin, make it this: a real cryptocurrency is defined by what no one can secretly control, and OneCoin controlled everything.

The three things that make a cryptocurrency real, and OneCoin faked all of them

You don't need to be technical to see the fraud. A genuine cryptocurrency rests on three pillars. OneCoin counterfeited each one.

How the money actually moved

OneCoin's real engine wasn't crypto — it was multi-level marketing. You didn't mainly make money when "the coin went up"; you made money, on paper, by recruiting other people to buy education "packages" that came with tokens to mine OneCoin. That structure is the classic shape of a pyramid: the returns shown to earlier members were funded by the money of later ones, not by any product or profit. When recruitment slows, the whole thing collapses — and around 2017, it did.

This is why the human cost was so wide. People didn't just lose their own money; they pulled in the people they trusted, because the scheme paid them to. That same dynamic — victims becoming unwitting recruiters — is what made OneCoin spread to more than a hundred countries, and it's why so many victims carry shame on top of loss. If that's you, it is worth saying plainly: falling for a scheme this engineered is not a failure of intelligence.

The people behind it, and where they are now

Unusually for a fraud this size, the courts have caught up with most of the inner circle. One person is the glaring exception.

Ruja Ignatova flew from Sofia to Athens on 25 October 2017 and has not been seen since. She remains on the FBI's Ten Most Wanted Fugitives list, with a U.S. reward of up to $5 million. The brains of the scheme, in other words, is still at large — while the people who sold it are still finding out what it cost them.

If you bought OneCoin

The story has one piece of genuinely good news. After authorities recovered funds tied to the fraud, a U.S. Department of Justice remission process opened to return money to eligible victims anywhere in the world — and it is free. The deadline is 30 June 2026, and the only official channel is onecoinremission.com.

And if you're wondering whether OneCoin is somehow still going, or whether a newer project that name-drops it is the real thing — we answer that here.

Got a "OneCoin recovery" message, or a new coin that sounds too good? Check it before you act.

Paste the email, the website, or the "agent" who contacted you. A real expert reviews every case and replies within 24 hours. Free, confidential, no pressure.

Common questions about OneCoin

What was OneCoin?

OneCoin was a fake cryptocurrency sold worldwide from 2014 as the 'next Bitcoin.' It was not a cryptocurrency at all. U.S. prosecutors describe it as one of the largest fraud schemes ever charged, with worldwide losses the Department of Justice puts at more than $4 billion. There was no real blockchain behind it: the 'coins' were numbers in a private company database, generated at will and given a price the company set itself. It was a Ponzi-and-pyramid scheme dressed as a tech revolution.

Why was OneCoin not a real cryptocurrency?

A real cryptocurrency runs on a public, independently verifiable blockchain that no single party controls, and it trades on open exchanges where the market sets the price. OneCoin had neither. According to the U.S. case against its operators, the coin ran on a central SQL database the company controlled — meaning the supply and the 'price' were whatever the operators typed in. It was never listed on any legitimate exchange, so members could almost never actually sell. Money flowed in through recruitment; very little ever flowed back out.

Who was behind OneCoin and what happened to them?

Ruja Ignatova, the founder known as the 'Cryptoqueen,' vanished in October 2017 and remains on the FBI's Ten Most Wanted Fugitives list, with a State Department reward of up to $5 million for information leading to her arrest. Co-founder Karl Sebastian Greenwood pleaded guilty and was sentenced to 20 years in prison. Mark Scott, a lawyer who laundered roughly $400 million for the scheme, was sentenced to 10 years, a conviction upheld on appeal in 2025. Ruja's brother, Konstantin Ignatov, pleaded guilty and cooperated; he was sentenced to time served in 2024.

How much money did OneCoin take, and how many victims?

The U.S. Department of Justice puts worldwide losses at more than $4 billion. Some coverage cites figures around $4.4 billion and as many as several million investors across more than 100 countries. The exact total may never be known because OneCoin's own records were the records of a fraud. What is not in dispute is the scale — this was a global scheme, not a local one.

I bought OneCoin and lost money. Can I get any of it back?

There is one legitimate, free route: a U.S. Department of Justice remission process returned recovered funds to eligible victims worldwide through onecoinremission.com. It covered people who bought OneCoin between 2014 and 2019 with a net loss, and it never charged a fee — but its filing window closed on 30 June 2026 and it is no longer accepting new claims. Be very careful: now that compensation is real, fraudsters are targeting OneCoin victims a second time, posing as 'recovery agents' who promise to unlock your payout for an upfront fee. That is always a scam. See our full guide to the compensation process for how to claim safely.

Sources & further reading

Claims in this piece are attributed to these sources. Click any of them to verify.