If you paid a scammer with a credit card, you hold the strongest recovery tool in consumer payments: the chargeback. The Fair Credit Billing Act lets you dispute a charge in writing within 60 days, and federal law caps your liability for unauthorized charges at $50 — usually $0 under Visa and Mastercard zero-liability rules. The key split: a card used without your permission is the easy case; a charge you were tricked into making yourself is harder, but still disputable as goods or services "not delivered as agreed." Call your issuer, name the dispute type correctly, and put it in writing.

"Federal law (the Fair Credit Billing Act, or FCBA) sets out a dispute process to help you get those mistakes fixed on credit cards … [you can dispute charges that] are things you didn't accept or weren't delivered as agreed. … Federal law limits your responsibility for unauthorized charges to $50."

— Federal Trade Commission, "Using Credit Cards and Disputing Charges." This dispute right is the one consumer-protection mechanism no other scam-payment rail has — which is why being pushed off a card is itself a warning.

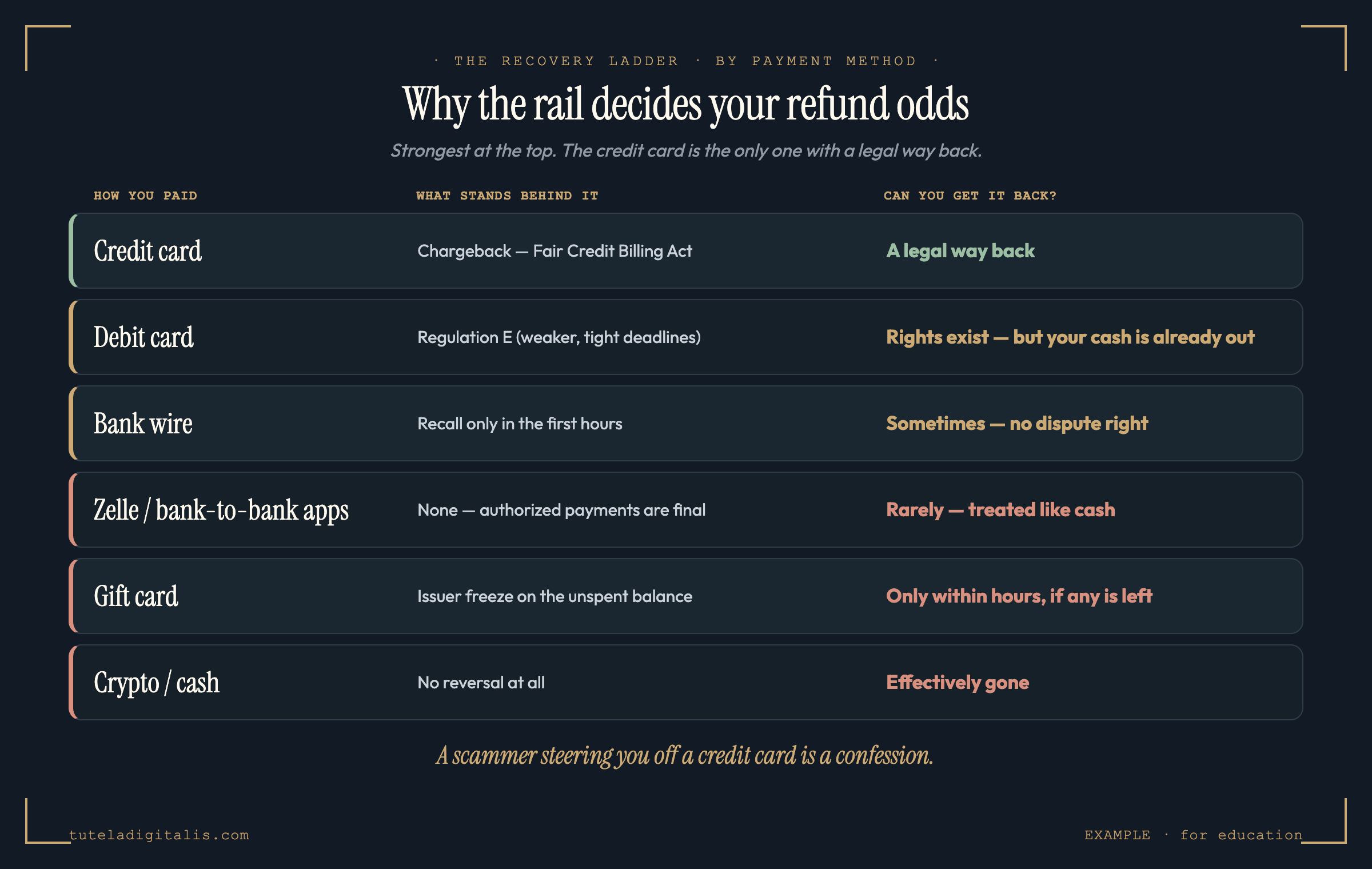

Here is the thing almost nobody tells you when you have just been scammed: the question "can I get my money back?" has already been half-answered by how you paid. A bank wire is hard to recall. Zelle is treated like cash. A gift card has only a freeze window measured in hours. Cryptocurrency is gone. The credit card is the exception — it is the only everyday payment method with a legal reversal right standing behind it. If your money left on a card, you are in the best position a scam victim can be in.

This is the credit-card version of the same recovery question that runs under every scam where money has already moved. The difference is the mechanism. With a gift card the lever is a freeze; with a credit card the lever is the dispute — and unlike the freeze, it does not expire in hours. But it is not automatic, and the words you use decide whether it works.

Why the credit card is the one rail with an undo button

Different payment methods carry completely different rights, and a scammer knows the ladder better than most victims do. Here is where the credit card sits, and why.

The two kinds of dispute, and which one you have

Everything about a credit-card scam recovery turns on one distinction, and using the wrong word can sink a winnable claim. There are two situations, and they are routed differently.

The mistake victims make is calling a deceived payment "unauthorized," getting denied because they clearly did authorize it, and assuming that's the end. It isn't. The correct frame is that you paid for something you never received, or that was misrepresented — a claim the law specifically lets you bring.

If you paid a scammer with a credit card, do this now

Work top to bottom. The first three steps decide most of the outcome; the rest protect you and build the record.

What to say to your bank: the words that work

The dispute is mostly a wording game. Be precise, be brief, and put it in writing. A few rules that decide how the claim is handled:

The UK and beyond, Section 75 and chargeback

Outside the US, the credit card is still the strongest rail, with its own rights. In the UK, Section 75 of the Consumer Credit Act 1974 makes your card provider jointly liable with the seller for purchases between £100 and £30,000 — so for a qualifying scam purchase you can claim against the card company directly. For amounts outside that range, or for debit cards, the voluntary chargeback scheme run by the card networks is the fallback. The principle is the same everywhere: a credit card puts a regulated institution between you and the loss in a way cash-like rails never do.

When a chargeback won't save you: the honest limits

A credit card is the best hand to be dealt, but it is not a guarantee. Be clear-eyed about where it stops.

So, can you get credit-card scam money back?

Often, yes — more often than with any other payment method, because the credit card is the one rail built with a reversal right inside it. An unauthorized charge is reversed routinely; a payment you were deceived into making is harder but genuinely disputable as goods or services not delivered as agreed. What decides it is speed, the right dispute wording, and your evidence — not how the scam made you feel.

And the deeper lesson is upstream of the refund: the safest way to pay any stranger is the rail that can take the money back. When someone tells you a card "won't work" and you must use a wire, a gift card, an app, or crypto instead, they are not solving a payment problem. They are removing your only undo button — and that, by itself, is the scam announcing itself.

If you take one rule from this whole piece, take this: a credit card is the only payment with a legal way back, so the instant you realize you've been scammed on one, call your issuer, name the dispute type correctly, and put it in writing within 60 days — and treat any demand to pay another way as the warning it is.

Paid a scammer with a card? Let's work the dispute together.

Tell us what happened, how much, and when — a real expert reviews every case and replies within 24 hours. Free, confidential, no judgment, nothing to sell.

Common questions about credit card scam refunds

Can you get your money back after paying a scammer with a credit card?

More often than with any other payment method — because the credit card is the only rail with a legal reversal right. The Fair Credit Billing Act lets you dispute a charge, and your issuer can run a chargeback to pull the money back from the merchant's bank. Two cases: a charge made without your permission (the card number was stolen and used) is the strong case — federal law caps your liability at $50, and most issuers charge you $0. A charge you were tricked into making yourself is harder, but still disputable as goods or services 'not delivered as agreed.' The deciding factors are how fast you report it, the dispute wording, and your evidence.

What's the difference between an unauthorized charge and one I was tricked into making?

It is the single most important distinction in a credit-card scam dispute. An unauthorized charge is one you never made — someone stole your card number and used it. Federal law limits your responsibility for unauthorized charges to $50, and Visa and Mastercard zero-liability rules usually drop that to $0, so these are reversed routinely. A charge you were deceived into authorizing is different: you entered your own card details because you were lied to. That is not 'unauthorized,' so do not call it that — frame it accurately as a charge for goods or services that were never delivered or were not as agreed, which the FCBA also lets you dispute. Using the wrong word gets the claim routed the wrong way.

How long do I have to dispute a credit card charge?

To keep your full federal protection, your written dispute has to reach the card issuer within 60 days of the first bill that showed the charge. Send it to the address for billing inquiries, not the payment address, and keep proof of delivery. Card-network chargeback windows are often longer (commonly up to 120 days, sometimes 540 for undelivered goods), but do not rely on the longer window — the 60-day FCBA deadline is the one that guarantees the law is on your side. The rule is simple: the moment you spot the charge, start the dispute.

Will my bank actually side with me in a scam chargeback?

Not automatically. A chargeback is an investigation, not a guarantee — the merchant's bank can contest it, and the outcome turns on your evidence and the dispute type. Unauthorized-use claims win most of the time. 'I was deceived into paying' claims are harder, because the merchant can argue you authorized the payment. What strengthens your case: report fast, dispute in writing, attach the messages and any fake invoice, show the goods or services never arrived or were not what you were promised, and keep every piece of correspondence. If the issuer rejects a clearly fraudulent charge, escalate a complaint to the CFPB.

The scammer told me to pay by Zelle, gift card, or crypto instead — why?

Because those rails have no chargeback. A scammer's choice of payment method is a confession: gift cards, cryptocurrency, wire transfers, and bank-to-bank apps like Zelle behave like cash and have no built-in reversal, while a credit card carries a federal dispute right they cannot get around. That is exactly why so many scams start on a card and then pressure you to 'switch' to another method, or insist from the start that a card 'won't work.' The request itself is the warning sign. If someone steers you off a credit card, assume the reason is that they know the card can take the money back.

Is a credit card dispute the same thing as a chargeback?

They are related but not identical. The dispute is your legal right under the Fair Credit Billing Act — the formal process where you tell your issuer a charge is wrong and they must investigate. The chargeback is the card-network mechanism (Visa, Mastercard, Amex rules) that your issuer uses to actually reverse the money and pull it back from the merchant's bank. In practice you start a dispute and, if it holds up, it results in a chargeback. You do not have to know the machinery — you just have to call your issuer, say you want to dispute a charge, and put it in writing within 60 days.

Sources & further reading

Every figure and instruction in this piece is drawn from these authorities. Click any of them to verify.