Facebook Marketplace itself is a real product, and most people use it without incident. The scams are run by other users, and they all share one structure: a maneuver to move you off the two safe defaults — meeting in person and paying with cash or verified funds, or keeping the deal inside Facebook’s protected checkout and chat — onto something irreversible: a gift card, a wire, a Zelle or Venmo Friends-and-Family transfer, a payment before you’ve seen the item, or a conversation moved off the platform. The tell is the deviation itself. Whenever the other side wants to do the deal a different way than normal, that is the scam asking to begin.

The item is bait. The rail is the target.

Almost every guide to Facebook Marketplace fraud hands you a list of scam names to memorize. That is the wrong mental model, because the names keep changing and the scripts keep evolving. The thing that never changes is the objective. A Marketplace scammer does not care about the couch. They care about getting money to move in a direction it cannot come back from.

There are only two genuinely safe ways to do a Marketplace deal. The first is to meet in person, in public, and pay cash — or hand over the item only after real, verified funds have landed in your own account. The second, for shipped items, is to stay inside Facebook’s own checkout and chat, where there is a payment record, a report button, and, on eligible orders, Purchase Protection. Both of those defaults are reversible or accountable. Every scam on the platform is a piece of theatre designed to talk you out of one of them.

So the map below is not organized by scam name. It is organized by who you are in the transaction — because Facebook Marketplace is the one place where the same con wears two different faces. The seller-side version and the buyer-side version are mirror images of each other, and once you can see both, the individual scripts stop being surprising.

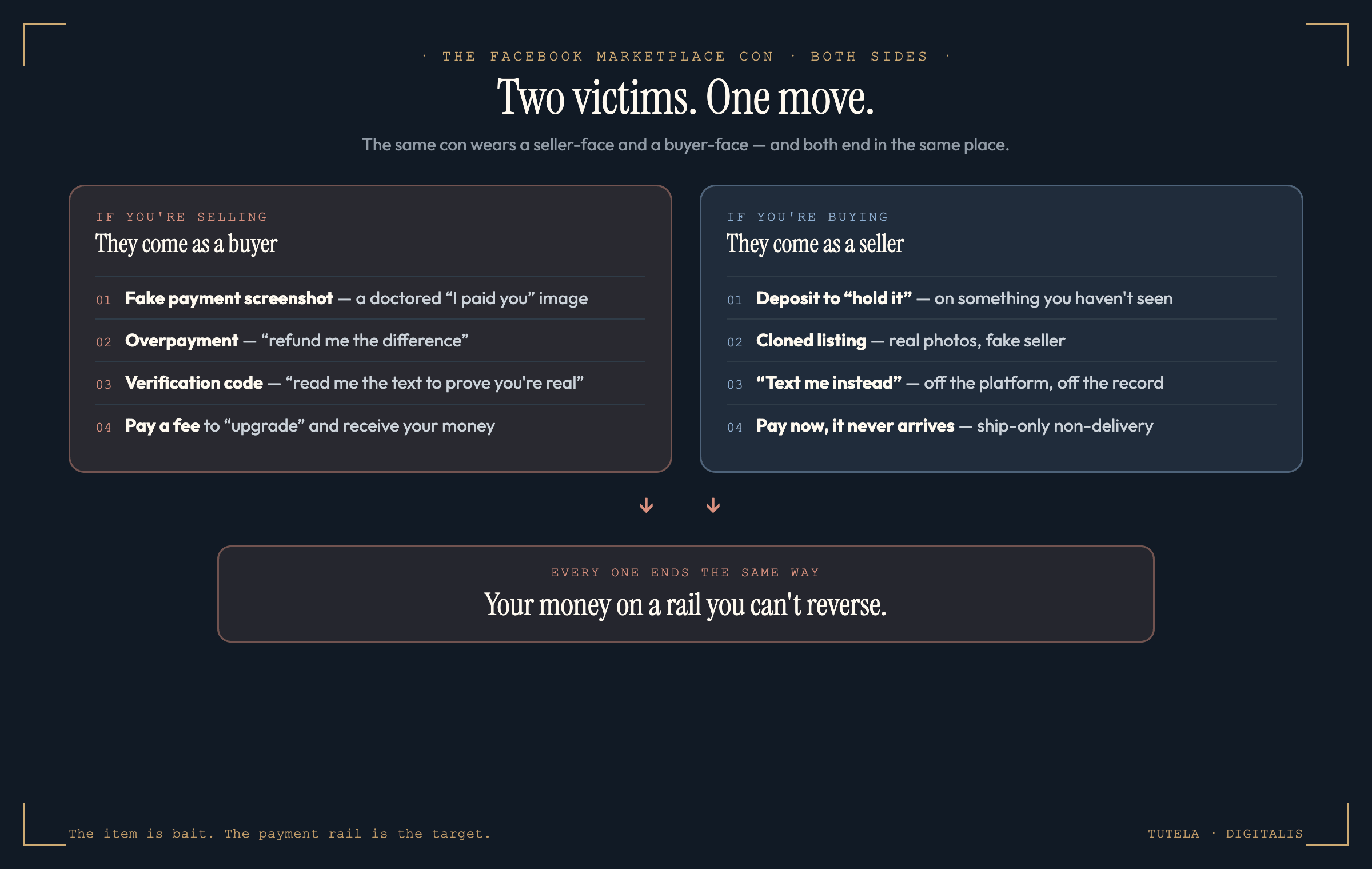

The mirror: the same con from both sides

Read your own side first, then read the other one — because the day you switch from selling your old bike to buying a used laptop, you become the other kind of target. Each move below comes with why it works and the one check that ends it.

A buyer messages “I just sent it, check your email” and pastes a screenshot of a Venmo, Zelle, or PayPal confirmation. The image is doctored in seconds. If you ship or hand over the item on the strength of a picture, the money was never real.

The buyer “accidentally” pays more than the price — a cashier’s check, or a transfer that can later be reversed — and asks you to refund the overage. The original payment bounces or is clawed back a week later. You are out the item and the overage.

A “buyer” texts you a six-digit Google code and asks you to read it back “to prove you’re a real seller.” Reading it back lets them create a Google Voice number in your name — or take over an account tied to your phone. It has nothing to do with the sale.

The buyer says their payment app requires you to have a business or upgraded account, then sends a fake “payment pending — pay a fee to release it” email dressed up as Venmo, Zelle, or PayPal. No payment is ever on hold; you are being asked to pay to “receive” money that does not exist.

The listing is a great price on an apartment, a car, a console, a puppy. The seller “has a lot of interest” and asks for a deposit to hold it — by gift card, Zelle, Venmo Friends-and-Family, or wire — before you see it. The item does not exist.

The photos are lifted from a real listing somewhere else. The “seller” collects payment and disappears — or “sells” the same one item to a dozen buyers. The pictures look perfect because they belong to someone who is not the person you are talking to.

Early in the chat the seller pushes you to “text me” or “message me on WhatsApp.” Off Marketplace there is no report button, no chat history, and no trail — exactly what they need before money moves. The move happens before any price is even agreed.

“Shipping only — pay first.” This is the single most-reported social-media shopping scam: most victims say the item never arrived, and the rest got a knockoff or the wrong thing entirely. The listing is designed to be paid for and then abandoned.

What the data says about where this happens

In April 2026 the FTC reported that Americans lost $2.1 billion to scams that began on social media in 2025 — eight times the 2020 figure, and more than any other way scammers reach people, including phone, text, and email combined. Facebook alone accounted for $794 million of it, the largest share of any platform. The most-reported scam type that started on social media was online shopping: more than 40% of people who lost money to a social-media scam said they had ordered something they saw in a post or ad, and most of them said the item simply never arrived.

Those numbers are why the payment-rail lens matters more than the scam-name lens. The losses are not concentrated in one exotic script — they are spread across dozens of variations that all end the same way, with money on an irreversible rail. Facebook publishes its own Marketplace guidance telling users to meet in person, use approved payment methods, and avoid deals that require gift cards or wires. The guidance is correct. The reason the scams keep working is that every one of them is engineered to give you a warm, plausible reason to ignore it.

If you already got scammed on Facebook Marketplace

Speed matters, and the payment method decides your first move. Work the rail you actually used:

Then report the listing inside Facebook and file at reportfraud.ftc.gov and ic3.gov. For the full first-hour sequence sorted by exactly what you paid with, use the just-got-scammed emergency tool, and see the 72-hour recovery playbook for the by-method odds.

The seven-step Marketplace playbook

None of this is exotic. It is the safe deal, written down, so that a warm and plausible stranger cannot talk you out of it in the moment.

So — is Facebook Marketplace safe?

Used inside its two safe defaults, yes. Meet in person, pay cash or verified funds, keep shipped deals on-platform through checkout, and the large majority of Marketplace scams cannot reach you — because they all depend on you stepping outside those defaults. The platform is not the danger. The danger is the moment a friendly stranger gives you a good reason to do it a slightly different way.

If you take one rule from this whole piece, take this: on Facebook Marketplace, the item is never the target — your payment rail is. The instant someone wants to move the deal off the platform, off a reversible payment, or ahead of you actually seeing the item, the deal is the scam. Slow down and go back to the safe default.

Already paid a Marketplace seller who’s gone quiet? Let’s look at the recovery path together.

Tell us the amount, the payment method, and the timeline. A real expert reviews every case and replies within 24 hours. Free, confidential, no pressure.

Common questions about Facebook Marketplace scams

How do I not get scammed on Facebook Marketplace?

Hold to two defaults and treat any push away from them as the warning sign. Default one: meet in person, in a public place, and pay with cash or only after verified funds land in your own account. Default two: if the item must ship, keep the entire deal inside Facebook’s chat and pay only through a rail that carries buyer protection. Almost every Facebook Marketplace scam is a maneuver to move you off one of those two defaults — to a gift card, a wire, a Venmo Friends-and-Family payment, a text conversation off the platform, or a payment before you’ve seen the item. The single question that stops most of them: why does this person want to do it a different way than normal?

What are the most common Facebook Marketplace scams?

They split cleanly into seller-side and buyer-side versions of the same con. If you are selling, the four dominant patterns are the fake payment screenshot, the overpayment “send the difference back” scam, the Google Voice verification-code scam, and the fake “pay a fee to receive your money” business-account upgrade. If you are buying, they are the deposit-to-hold on a listing that does not exist, the cloned or stolen listing, the push to move the chat off Facebook, and the pay-before-you-see non-delivery scam. Underneath all eight is one mechanic: get you off the safe way of doing the deal and onto a payment or channel you cannot reverse.

I got scammed on Facebook Marketplace — what can I do?

Move fast, and let the payment method decide your first call. If you paid by credit or debit card, or through Facebook’s own checkout, dispute the charge with your card issuer and check whether Purchase Protection applies. If you paid by Venmo or Cash App Goods and Services, open an in-app dispute; if you paid Friends and Family, go around the app to the bank or card that funded it and dispute under Regulation E or the Fair Credit Billing Act. Zelle payments should be reported to your bank immediately. Gift-card and wire payments need a call to the gift-card company or your bank right away — sometimes a wire can still be recalled within a short window. Then report the listing to Facebook and file at reportfraud.ftc.gov and ic3.gov. Our step-by-step tool at /just-got-scammed walks the first hour by payment method.

Are Facebook Marketplace Venmo scams real, and should I use Venmo there?

They are among the most common Marketplace scams, and the safe way to use Venmo is narrow. The danger is Venmo’s Friends and Family tag, which has no buyer protection and cannot be reversed — exactly what scammers ask for. If you buy or sell on Marketplace with Venmo, use Goods and Services or a Business-profile payment, never Friends and Family with a stranger, and never release an item or refund an “overpayment” until real funds show in your own Venmo activity feed. A screenshot of a payment is not a payment. The same logic applies to Cash App and Zelle, which have even less recourse than Venmo Goods and Services.

Why do Facebook Marketplace buyers or sellers ask to text or use WhatsApp?

Because moving off Facebook removes the guardrails. Inside Marketplace chat there is a report button, a message history, and a record tied to the listing. Over text or WhatsApp none of that exists, and the person can delete themselves the moment the money moves. Legitimate local deals almost never need to leave the platform before you meet. When a buyer or seller pushes to take the conversation to text, email, or WhatsApp before anything is agreed, treat it as the first move of the scam, not a convenience.

Is it safe to pay a deposit on Facebook Marketplace?

No — not to hold an item you have not seen in person. “Send a deposit so I can hold it for you” is one of the most reliable Marketplace scam scripts, especially on apartments, cars, and in-demand electronics. The deposit is almost always requested on an irreversible rail: gift card, wire, Zelle, or Venmo Friends and Family. There is no item and no hold. Pay for a local item only when you are standing in front of it, and pay a shipped item only through a method with buyer protection.

Does Facebook Marketplace have buyer protection or refund scams?

Only in a narrow case. Purchase Protection can apply to eligible orders bought and shipped through Facebook’s own checkout and paid on-platform — those may qualify for a refund if the item never arrives or is badly misdescribed. The moment a deal moves to cash in person, or to an off-platform payment like Zelle, Venmo Friends and Family, gift cards, or a wire, Facebook’s protection does not apply and there is no refund from Meta. That gap is exactly why scammers work so hard to move you off the platform and off protected payments. If you were scammed, recovery runs through the payment rail you used, not through Facebook.

Sources & further reading

Every figure in this piece is drawn from these authorities. Click any of them to verify.